SOPHIA ANTIPOLIS, France – January 12, 2017| 3D is becoming a key technology platform for increase integration, either for heterogeneous integration (like for MEMS and CMOS image sensor) or for increasing the performances (like for DRAM and IC partitioning). When a company has started to adopt TSV, there is no turning back.

In 2016 again, both market segments, high end and low end, were the main targets of the TSV technologies providers. In its latest advanced packaging technology and market analysis entitled 3DIC and 2.5D TSV Interconnect for Advanced Packaging: 2016 Business Update report, Yole Développement (Yole) announces, high volume production started: 3D TSV is a reality, especially in the memory industry… Amongst a dynamic advanced packaging market showing an overall advanced packaging revenue CAGR estimated at 8%, rising to US$ 30 billion in 2020, the development of TSV platforms is still pushed by the need to the increase of performance, functionalities and integration; in addition, form factor and cost reduction are also part of the playground. The More than Moore market research and strategy consulting company proposes today an overview of the 3D/2.5D IC packaging technologies per application. In addition to wafer forecast for 2015-2021 for different TSV applications, Yole’s analysts will review the status of the current and future 3D IC products, the teardown of the major products using TSV in 2016 (including the evolution of Sony stacking technologies) and the patent trends. They also will describe and analyze the dedicated technology roadmap per device and highlight the organization of this market including supply chain activities, list of key players and OSAT and foundry strategies. 3D TSV technology is becoming a key solution platform for heterogeneous interconnection, high end memory and performance applications. The webcast ‘TSV technology: a key platform for heterogeneous integration’, hold on January 16, will mix market, technology and patent analysis from Yole Développement, System Plus Consulting and KnowMade, all part of the Yole Group of Companies.

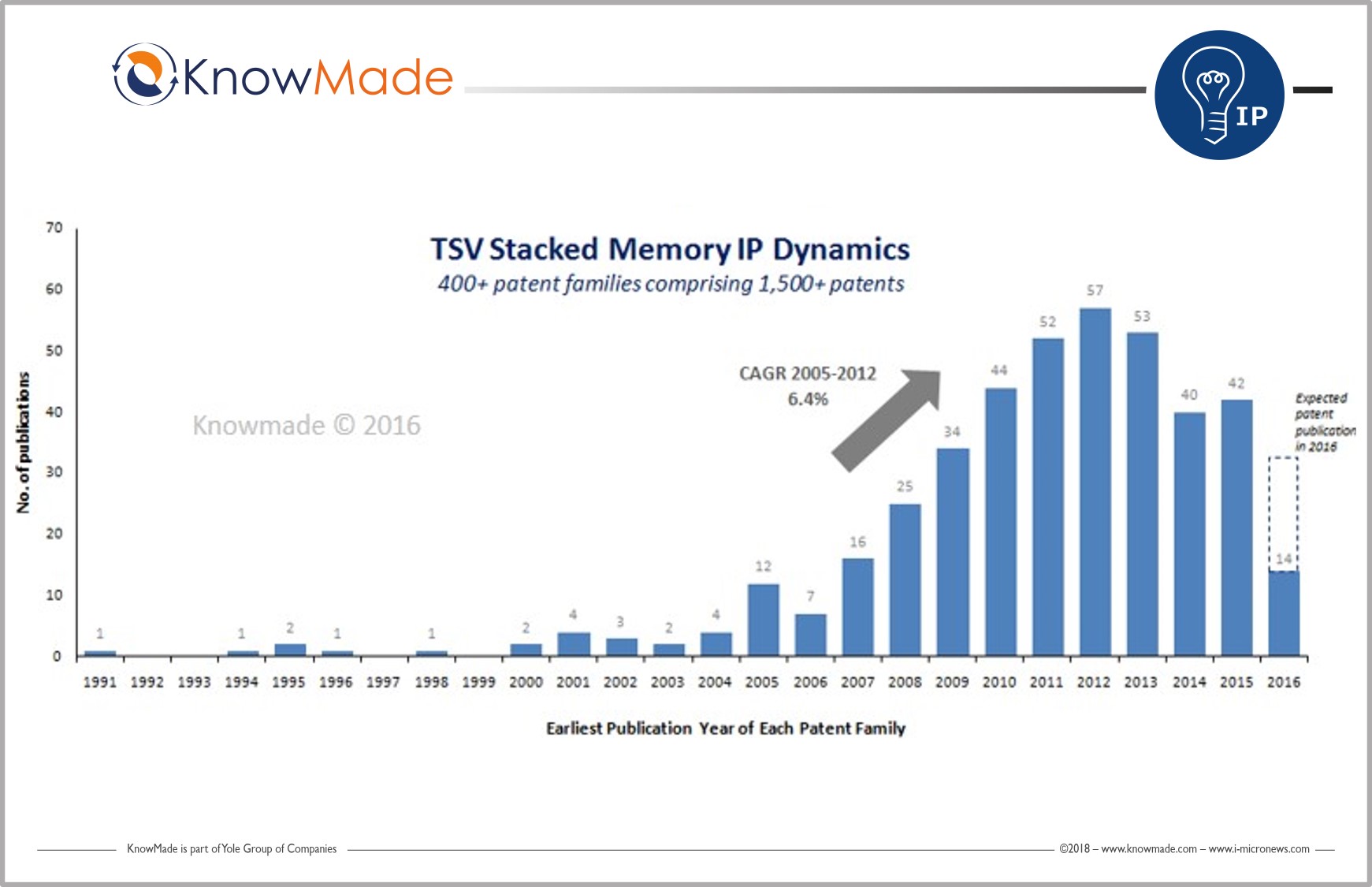

On the patent side, the last years have been very active. Indeed, since mid-2000s, more than 400 patents families relating to TSV stacked memory technology have been published according to TSV Stacked Memory Patent Landscape Analysis from KnowMade, a technology intelligence and IP strategy consulting company. In parallel to the increase of the patent activities, the last two years have showed some important changes within the 3D TSV memory market. First commercial products patent litigations took place between ELM 3DS and leaders such as Samsung Electronics, SK Hynix and Micron Technology. From the market point of view, the higher end market segment is led by 3D stacked memories, 2.5D integration and emerging application such as photonics. From its side, the low end application includes CIS, MEMS devices and other sensors and new applications such as LEDs. TSVs have now become the preferred interconnect choice for high-end memory. They are also an enabling technology for heterogeneous integration of logic circuits with CIS, MEMS, sensors, and RF filters. In the near future they will also enable photonics and LED function integration.

“The market for 3D TSV and 2.5D interconnect is expected to reach around 2.1 million wafers in 2021, expanding at an 18% CAGR”, asserts Santosh Kumar, Senior Technology& Market Analyst at Yole. The growth is driven by increased adoption of 3D memory devices in high-end graphics, high-performance computing, networking and data centers, and penetration into new areas, including fingerprint and ambient light sensors, RF filters and LEDs.

For example an HBM has been introduced by AMD in its Radeon™ R9 Fury X high-end graphics card. System Plus Consulting released in 2015 a detailed reverse engineering and costing analysis of this component, titled AMD World’s First HBM-Powered Product SK Hynix 3D TSV High-Bandwidth Memory and highlighting 3D TSV technology added-value in this new component: “AMD’s 3D & 2.5D component integrates HBM such as DRAM dies & logic dies connected with via-middle 3D TSV and micro-bumps as well as GPU stacked onto a silicon interposer including also via-middle 3D TSV,” explains Romain Fraux, CTO’s System Plus Consulting. According to AMD, this HBM component delivers 60% more memory bandwidth, 3 x the performance per watt and consumes 94% less PCB area than GDDR5.

Moreover, both AMD and Nvidia have also announced new graphics products exploiting next generation HBM2 technology. Other announcements include networking OEMs such as Cisco and Juniper Networks with switches and routers integrated with HMC and HBM technology. And memory suppliers SK Hynix, Samsung and Micron have already announced the specification for third generation HBM3 and HMC3. Another important market is 3DS DDR4, for servers. Yole’s analysts believe that the market share of 3DS could surpass other 3D memories in next 10 years. Samsung and SK Hynix are already in high-volume manufacturing with 3DS products and Micron too will soon enter this market.

CIS still commanded more than 80% share of TSV market wafer volume in 2015, although this will decrease to around 56% by 2021. This is primarily due to the growth of the other TSV applications, led by 3D memories, RF filters and fingerprint sensors. However, hybrid stacked technology, which uses direct copper-copper bonding, not TSVs, will penetrate around 38% of CIS production by 2021. The TSV markets for RF filters and fingerprint sensors are expected to reach around US$2.6 billion and US$0.7 billion by 2021 respectively.

Under this new report, Yole’s analysts also highlight the diversity of business models within the 3D & 2.5D TSV supply chain.

Si interposers suppliers, 3D packaging foundries and R&D services are also part of the business models identified by Yole’s analysts.

So will 3D TSV open the doors for new strategies? Indeed each player has its own approach:

- Both OSATs, Amkor Technology and SPIL are strongly involved in the memory and the MEMS & Sensor market.

- In parallel Samsung, an IDM, is well positioned in the CIS, Si interposer and LED market segments only.

- In addition no foundries for memory products have been identified by Yole’s advanced packaging team.

Amongst the numerous 3D & 2.5D TSV players, Micron, SKHynix, Samsung, AMS and Avago Technologies are investing in capex… A detailed analysis per player is available in Yole’s report, especially the OSATs and foundries strategies, that are willing to increase their market shares for TSV applications.

3DIC & 2.5D TSV continue its attractive growth. Under a dynamic ecosystem, a lot of valuable companies are involved in this field and propose innovative solutions. Because of the increasing consumer market, as well as the need for higher performance products such as 4K gaming, networking, 2.5D/3D TSV packaging platform becomes a key solution platform.

KnowMade realizes various patent landscape reports on memory technology. Let’s discover them!

Press contact

contact@knowmade.fr

Le Drakkar, 2405 route des Dolines, 06560 Valbonne Sophia Antipolis, France

www.knowmade.com

About Knowmade

Knowmade is a Technology Intelligence and IP Strategy consulting company specialized in analysis of patents and scientific information. The company helps innovative companies and R&D organizations to understand their competitive landscape, follow technology trends, and find out opportunities and threats in terms of technology and patents.

Knowmade’s analysts combine their strong technology expertise and in-depth knowledge of patents with powerful analytics tools and methodologies to turn patents and scientific information into business-oriented report for decision makers working in R&D, Innovation Strategy, Intellectual Property, and Marketing. Our experts provide prior art search, patent landscape analysis, scientific literature analysis, patent valuation, IP due diligence and freedom-to-operate analysis. In parallel the company proposes litigation/licensing support, technology scouting and IP/technology watch service.

Knowmade has a solid expertise in Compound Semiconductors, Power Electronics, Batteries, RF Technologies & Wireless Communications, Solid-State Lighting & Display, Photonics, Memories, MEMS & Solid-State Sensors/Actuators, Semiconductor Manufacturing, Packaging & Assembly, Medical Devices, Medical Imaging, Microfluidics, Biotechnology, Pharmaceutics, and Agri-Food.