SOPHIA ANTIPOLIS, France – May 17, 2022 | The Silicon Carbide (SiC) power device market is growing fast, driven by the adoption of SiC technology in EV applications. SiC power device market revenues exceeded $1 billion in 2021 and were generated by companies mainly located in Europe (STMicroelectronics, Infineon), in the US (Wolfspeed, onsemi) and in Japan (Rohm Semiconductor, Mitsubishi Electric, Fuji Electric). What’s more, Yole Développement recently forecasted a multi-billion dollar SiC power device market over the coming years, exceeding $6 billion in 2027 with an estimated CAGR of 34% in 2021-2027. Obviously, the other major nations in the semiconductor industry, including China, South Korea and Taiwan, have unveiled their ambitions to develop their own SiC industry. Yet their ability to build the whole supply chain required for power SiC technology in the short- or mid-term has been questioned, especially regarding the establishment of a domestic supply for SiC wafers. Indeed, the entry barrier in the SiC wafer business is remarkably high, as evidenced by the very limited number of companies currently able to mass-produce large-area, high-quality SiC wafers for power device makers, so that they can comply with the stringent device requirements expected from the EV industry.

Patent landscape analysis is a powerful tool for identifying new players in emerging industries long before they enter the market, while providing a better understanding of their expertise and know-how in a specific technology. Overall, patenting activity (patent filings) reflects the level of R&D investment made by a country or player in a specific technology, while providing clues as to the technology readiness level reached by the main IP players. What’s more, the technology coverage along the value chain and the geographical coverage of the patent portfolios are closely related to the business strategy of IP players.

As such, Knowmade has applied patent landscape analysis to power SiC technology, providing in-depth analysis of established and emerging SiC semiconductor ecosystems, published in its latest Power SiC report released in May 2022. Furthermore, Knowmade published a previous article in January 2022 focusing on the Chinese Power SiC patent landscape. Just like in China, significant R&D efforts have been funded by the South Korean government to build a SiC industry over the existing domestic infrastructure, as highlighted by Veliadis et al. in an article published in 2019. Recently, the South Korean semiconductor industry has made important moves, including M&As (SK / Yes Powertechnix), acquisition of SiC assets (LG Innotek / LX Semicon), and new spin-offs (SKC / Senic), sketching the outlines of a future domestic SiC supply chain in South Korea.

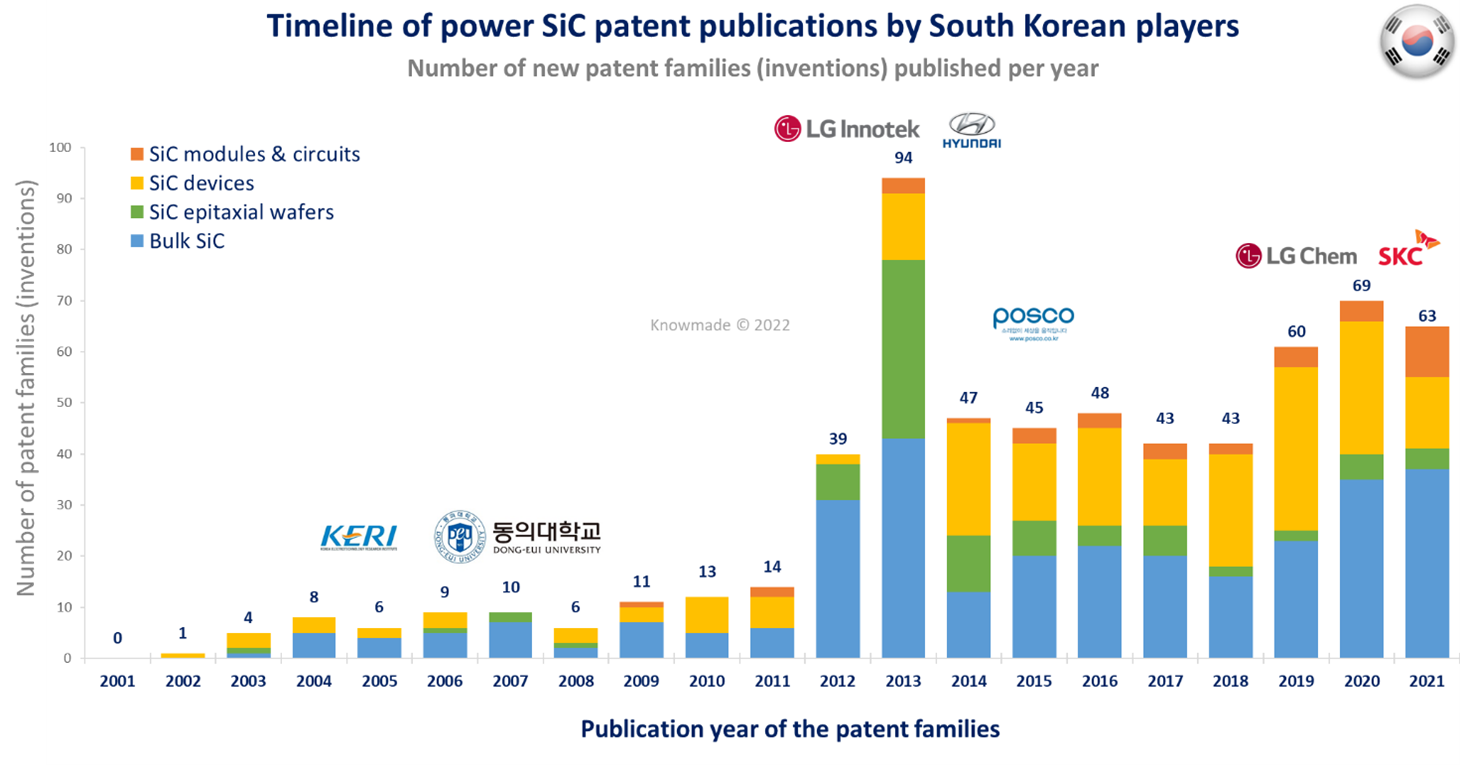

The patent analysis describes two decades of patenting activity related to SiC technology in South Korea. In the 2000s, the South Korean Power SiC patent landscape was dominated by the Korea Electrotechnology Research Institute (KERI), which published nearly 20 new inventions over the decade, and Dong-EUI University, which published more than 10 inventions related to bulk SiC crystal growth by sublimation between 2004 and 2010. In 2012, patenting activity took off in South Korea, peaking in 2013, driven by LG Innotek, actively engaged in the development of SiC crystal growth by sublimation and SiC epitaxy by chemical vapor deposition, and Hyundai Motor, focusing on SiC MOSFET technology (Figure 1). Overall, South Korean patenting activity has been dominated by SiC substrate development, with more than 380 inventions (of which 80+ inventions related to SiC epitaxial wafers); and SiC power devices, with more than 210 inventions, focusing on SiC MOSFET (120+ inventions, of which 70+ related to SiC trench MOSFET). So far, South Korean IP players have filed few SiC module and SiC circuit patents (less than 40 inventions), the first patent applicant being Hyundai Motor / Kia Motors since 2016.

Figure 1: Timeline of patent publications by South Korean players in the power SiC patent landscape.

The rise in SiC substrate patent applications is concomitant with the World Premier Materials project funded by the South Korean government between 2009 and 2019 to develop SiC substrate technology. The project was led by POSCO, which established 4-inch and 6-inch 4H-SiC substrate technology, and LG Innotek, which established commercial-grade 6-inch SiC epitaxial wafers for power applications. These achievements resulted in significant patenting activity in the SiC substrate patent landscape from LG Innotek (2012-2014) and from POSCO (2014-2017), as shown in Figure 1. In recent years, several IP challengers appeared in the bulk SiC patent landscape, such as SKC, a well-established IP player which published more than 30 patents in 2020/2021, and LG Chem, a relatively new IP player entering the patent landscape in 2017, which has published more than 40 patents so far. Interestingly, while most South Korean patent applicants focus on sublimation growth for producing bulk SiC, LG Chem is developing the solution growth technique. Accordingly, LG Corporation has access to complementary patent portfolios, covering both growth techniques for SiC substrate technology.

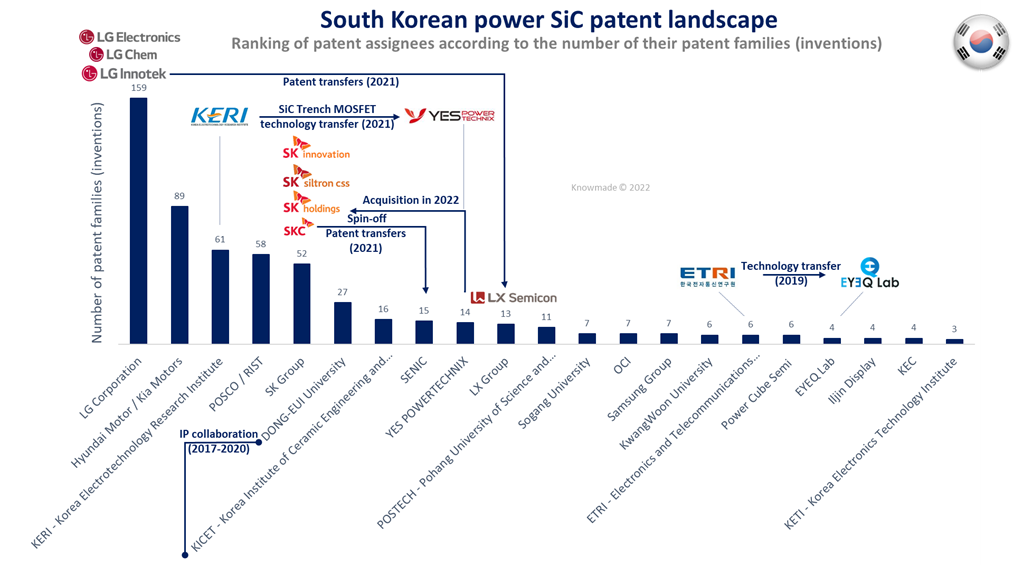

Figure 2: Ranking of South Korean IP players in the power SiC patent landscape.

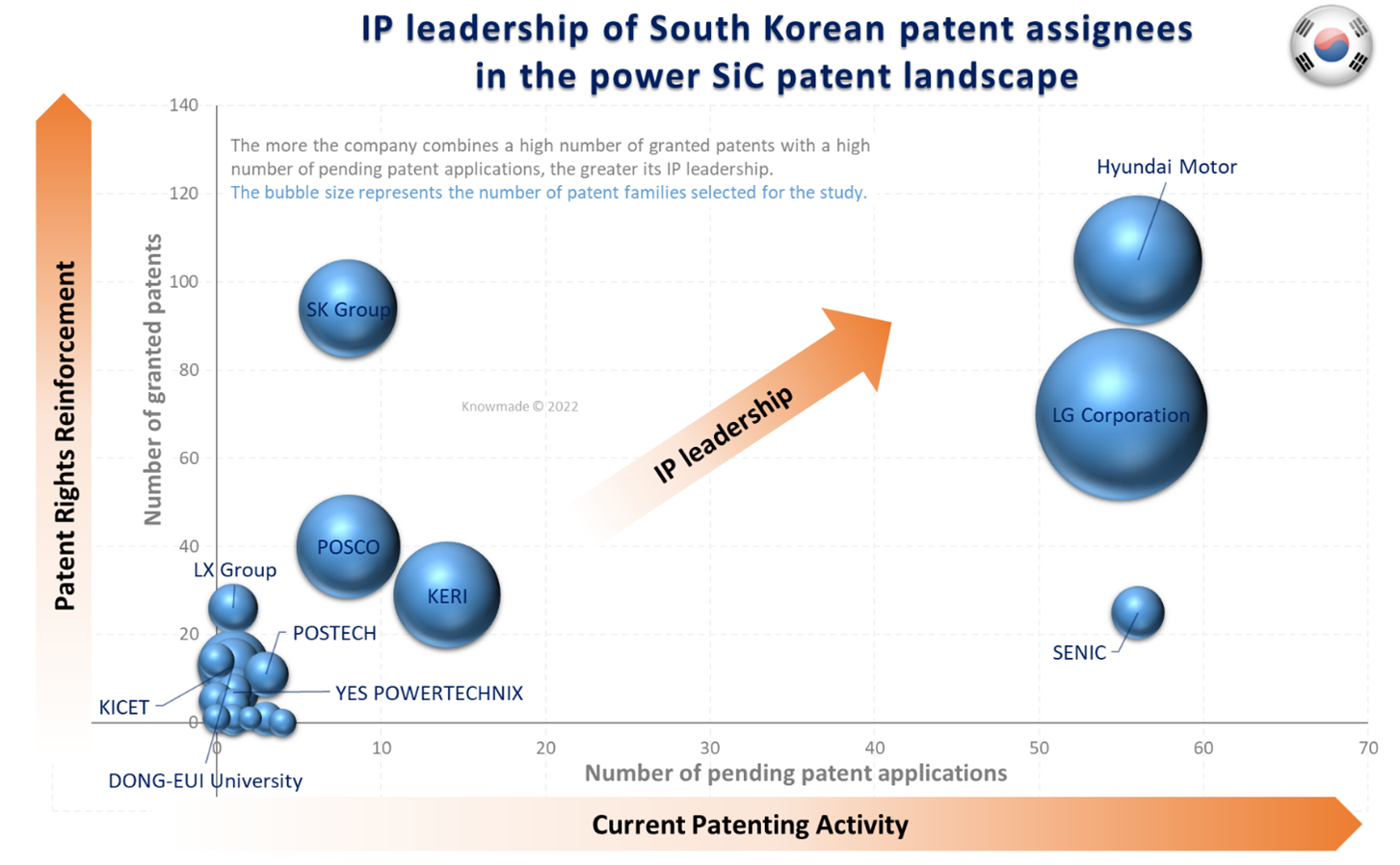

LG Corporation (which includes LG Chem, LG Electronics, and its subsidiary LG Innotek) holds the largest patent portfolio (in terms of number of inventions) among South Korean patent assignees in the power SiC IP landscape (Figure 2). LG demonstrates strong IP leadership in the power SiC patent landscape, holding a significant number of granted patents, combined with a high number of pending patent applications, similar to that of Hyundai Motor (Figure 3). The high number of pending patent applications relates to LG Chem’s recent patenting activity in the field of bulk SiC solution growth. As of May 2022, most SiC substrate patents assigned to LG are South Korean patents (domestic patents). In 2018, LG Electronics entered the SiC power device patent landscape (Figure 4), publishing four SiC planar MOSFET inventions. It confirms the onset of internal developments regarding SiC technology, to establish a vertical innovation strategy in the LG group. In May 2021, LG spun off LX Group, including five LG subsidiaries, among which is Silicon Works, now LX Semicon, the first fabless chip maker in South Korea, specializing in display driving chips. In December 2021, LX Semicon acquired LG Innotek’s tangible and intangible SiC assets, to develop SiC semiconductors and enter the semiconductor market for automotives. As of May 2022, more than 20 patents have been transferred to LX Semicon, which relate to SiC epitaxial wafers. Most patents are granted, mainly in the US and South Korea (Figure 3). Accordingly, LX Semicon is now engaged in the development of power SiC technology, starting with SiC epiwafers based on the technology developed by LG Innotek.

Figure 3: IP leadership of South Korean patent assignees in the power SiC patent landscape.

In 2020, semiconductor wafer maker SK Siltron, a subsidiary of SK Group, acquired US DuPont’s SiC Wafer division, now SK Siltron CSS, which has been developing SiC substrate technology since the early 2000s. SK Siltron CSS owns several key patents in the field of bulk SiC as well as SiC epiwafers, and is developing 8-inch SiC substrate technology. On the other hand, another SK Group subsidiary SKC spun off its SiC wafer business, establishing Senic in 2021. As of 2022, more than 20 patents related to bulk SiC crystal growth (using the sublimation growth technique) were transferred from SKC to Senic in 2021 (Figure 2 includes data up to August 2021). As shown in Figure 3, most patents in Senic’s portfolio are pending, and the high number of patents (80+) compared to the number of inventions (15) can be explained by a global patenting strategy: most patent families/inventions are filed in multiple countries (including USA, Europe, China, Japan and Taiwan). Most SKC patents that have not been transferred to Senic are domestic granted patents, but SK’s remain well positioned in the global IP landscape thanks to SK Siltron CSS’ patent portfolio, mainly made up of granted patents covering the three major semiconductor markets for power SiC (USA, Europe, China). In 2022, SK Group acquired Yes Powertechnix (YPT), a SiC power semiconductor IDM company offering a foundry service, established in 2017, which acquired the SiC trench MOSFET technology from KERI in 2021. Overall, KERI has filed more than 50 SiC device patents, of which 10 describe SiC trench MOSFET technology. Most of KERI’s SiC device patents are domestic patent applications. However, recent PCT applications may indicate a change in KERI’s IP strategy (WO2021/049801, WO2018/208112, WO2018/194336).

Yes Powertechnix, which entered the SiC power device patent landscape in 2019, has already published 14 SiC device inventions, of which several patents covering the trench MOSFET technology. However, about half of patent applications are already dead (revoked), and YPT’s patenting activity has been limited to South Korea so far, explaining its position in Figure 3.

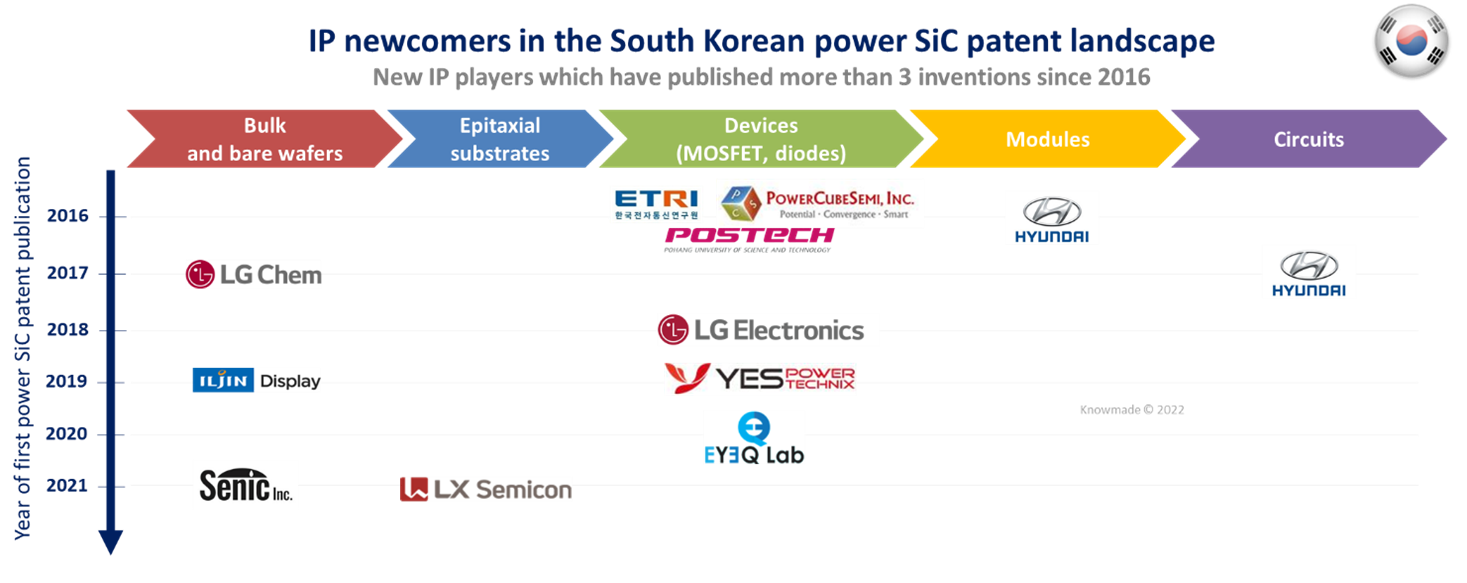

Figure 4: IP newcomers vs. SiC supply chain since 2016.

Hyundai Motor positions itself as the main IP leader in the SiC power device patent landscape, focusing on SiC trench MOSFET technology. Hyundai Motor’s SiC patent portfolio features the highest numbers of granted and pending patents among South Korean patent assignees. Furthermore, its patent portfolio has good geographical coverage outside South Korea, including China and USA. According to its recent patenting activity, the OEM company is now strengthening its IP position in Europe and China. Today, Hyundai relies on Infineon’s CoolSiC power modules (based on SiC trench MOSFET) for its EV platform E-GMP. Several Hyundai power module patents related to EV applications were co-filed with Infineon

in 2016/2017. In addition, the first SiC module and SiC circuit patents have been published by Hyundai in 2016/2017, indicating that the OEM has internal developments to address integration challenges related to SiC technology. Having developed strong expertise in both EV technology and SiC semiconductor technology, from device to modules and circuits, Hyundai Motor should play a key role in the establishment of the domestic SiC supply chain (Figure 5).

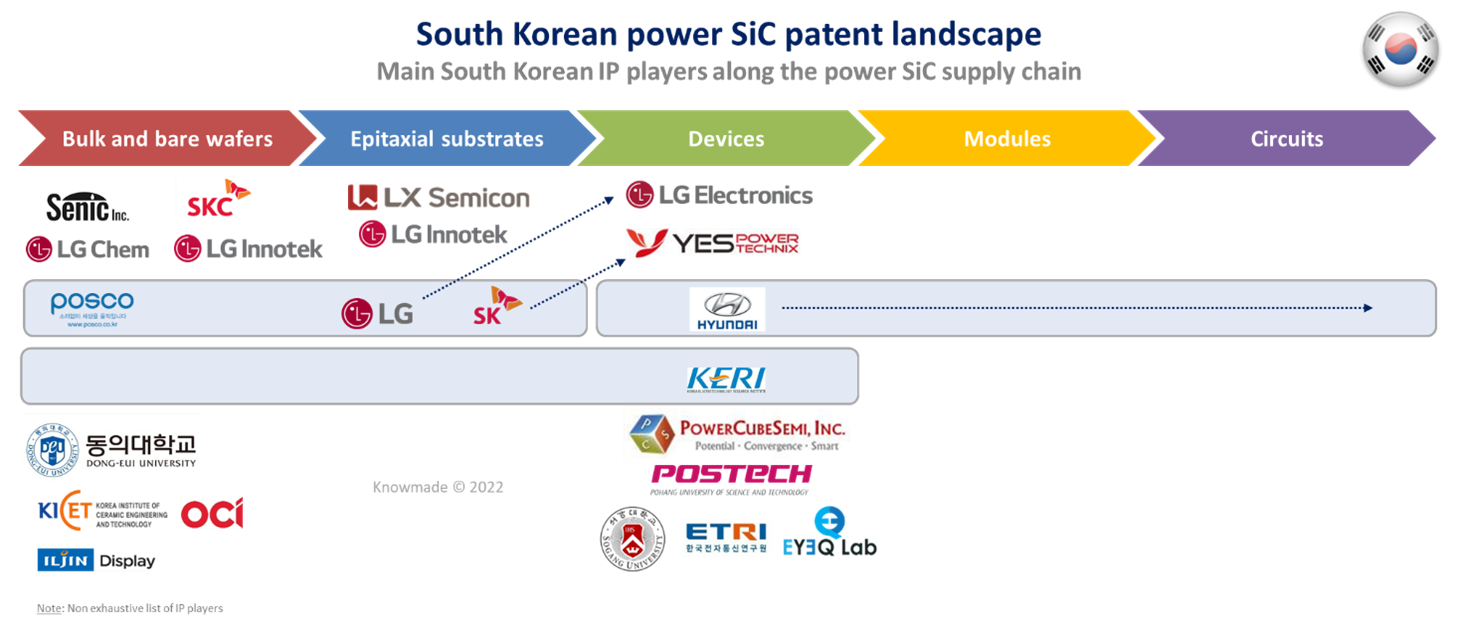

Figure 5: Main IP players vs. SiC supply chain

Conclusion – The role of the main IP players in the emergence of a SiC industry in South Korea is well explained by the patent analysis. SK, LG and POSCO took the lead in developing SiC substrate technology, while KERI and then Hyundai Motor have been driving the development of SiC power devices. All together, their patenting activity is covering the whole supply chain for SiC technology. Today, LG remains the main innovator for SiC substrate technology according to the large technological coverage of its patent portfolios, but its IP strategy does not indicate it will play a major role in establishing a supply chain for the emerging SiC industry or developing a SiC business in South Korea. In this regard, SK Group has developed an interesting strategy. First, its subsidiary SK Siltron has combined its know-how and expertise in semiconductor wafer manufacturing with external innovation brought by the acquisition of a well-established US IP player in SiC substrate technology. Next, its subsidiary SKC developed SiC crystal growth technology and spun off a new specialist company, Senic, with a view to strengthening domestic SiC wafer supply in the future. With a patent portfolio that aims to cover all major markets for power SiC technology, it is clear that Senic’s ambitions are not limited to the South Korean market. Finally, SK acquired SiC IDM and foundry Yes Powertechnix (YPT), which can produce a double effect on the South Korean SiC ecosystem. Firstly, SK enhances its capability to compete in the South Korean SiC power device market with leading foreign suppliers, leveraging the advantages of being a vertically integrated company. Secondly, it can strengthen the domestic supply chain by developing YPT’s foundry service, based on the synergy with its subsidiary SK Hynix. Indeed, most newcomers in the power SiC patent landscape are fabless chip makers with R&D facilities only (Power Cube Semi, EyeQ Lab, LX Semicon). Therefore, foundries are expected to play a key role in the development of the South Korean SiC industry, in contrast with USA, Europe or Japan, where IDM companies took the lead in SiC power device manufacturing. Furthermore, the main IP player in the SiC power device patent landscape is an OEM, Hyundai Motor, which is also the only player in this field with a global IP strategy. Overall, the patent landscape analysis shows that few South Korean players have built a significant patent portfolio abroad, which will certainly limit their international ambitions. Furthermore, the analysis points out that, according to the number of inventions, few South Korean players are engaged in SiC power modules and SiC circuit development. This might limit them in addressing certain applications such as EV technology, where power modules are generally preferred to discrete devices. Yet according to recent patenting activity, Hyundai Motor is trying to fill the gap in the South Korean downstream SiC supply chain.

While the present article focuses on South Korean patent assignees, Knowmade’s Power SiC report 2022 highlights several foreign IP players with sizeable patent portfolios in South Korea (Toyota / Denso, Showa Denko, Nissan), including major SiC power device market players (Mitsubishi Electric, Wolfspeed). Furthermore, other leading SiC power device makers are currently increasing their patent filings in South Korea (onsemi, Infineon), confirming a significant interest in the South Korean market.

KnowMade observes technology with patent landscape reports about power electronics devices.

Press contact

contact@knowmade.fr

Le Drakkar, 2405 route des Dolines, 06560 Valbonne Sophia Antipolis, France

www.knowmade.com

About our analysts

Rémi Comyn, PhD, Rémi works for Knowmade in the field of Compound Semiconductors and Electronics. He holds a PhD in Physics from the University of Nice Sophia-Antipolis (France) in partnership with CRHEA-CNRS (Sophia-Antipolis, France) and the University of Sherbrooke (Québec, Canada). Rémi previously worked in compound semiconductors research laboratory as Research Engineer.

About Knowmade

Knowmade is a Technology Intelligence and IP Strategy consulting company specialized in analysis of patents and scientific information. The company helps innovative companies and R&D organizations to understand their competitive landscape, follow technology trends, and find out opportunities and threats in terms of technology and patents.

Knowmade’s analysts combine their strong technology expertise and in-depth knowledge of patents with powerful analytics tools and methodologies to turn patents and scientific information into business-oriented report for decision makers working in R&D, Innovation Strategy, Intellectual Property, and Marketing. Our experts provide prior art search, patent landscape analysis, scientific literature analysis, patent valuation, IP due diligence and freedom-to-operate analysis. In parallel the company proposes litigation/licensing support, technology scouting and IP/technology watch service.

Knowmade has a solid expertise in Compound Semiconductors, Power Electronics, Batteries, RF Technologies & Wireless Communications, Solid-State Lighting & Display, Photonics, Memories, MEMS & Solid-State Sensors/Actuators, Semiconductor Manufacturing, Packaging & Assembly, Medical Devices, Medical Imaging, Microfluidics, Biotechnology, Pharmaceutics, and Agri-Food.

One thought on “Power SiC patent landscape analysis: who is driving the establishment of the SiC industry in South Korea?”

Comments are closed.